Greetings from the community foundation, and happy February!

In this month of Valentine’s Day when many people reflect on those they love, many fund holders at the Morton Community Foundation also reflect on the causes they care about and the organizations in our community they love. Many people use their donor-advised fund at the community foundation to make gifts to charity to celebrate Valentine’s Day, which is a bigger holiday for giving than many people realize. Americans spend $26 billion on Valentine’s Day gifts ($2 billion on pets!), including sending 145 million cards and 250 million roses.

In this newsletter we announce our 2024 Community Grants and Scholarships, and we show how you can show the love for the charities you care about the most:

Estate planning might feel like a burden on your to do list, but it’s actually one of the best ways you can show you care. Your loved ones, and the charities you care about, will appreciate your careful planning. And you’ll enjoy peace of mind knowing that you’ve got the documents in place to carry out your wishes, well before it’s needed. The Morton Community Foundation is happy to work with you and your advisors to structure a charitable giving legacy plan to achieve your goals for caring about the community you love.

At the Morton Community Foundation, we know that every gift matters. Whether you’ve established a donor-advised fund to carry out your annual giving to many different charities, or you’ve set up an unrestricted legacy fund to support our community’s greatest needs, you’ll be making a difference. The importance of every act of charity is a good reminder as you start implementing your charitable giving plans for 2024.

Fund holders and legacy donors at the Morton Community Foundation are often surprised to learn how the MCF can be involved in estate administration when a donor leaves a bequest. Our goal is to ensure that your charitable intentions are achieved, from structuring a bequest all the way through to the dollars flowing to the causes you care about the most.

The MCF offers so many tools and services to help you support the causes you care about. We’re honored to work with so many dedicated fund holders, and we are excited to work with so many of you who are considering establishing a fund at the Morton Community Foundation to pursue your own philanthropic passions. If you want to read more about the over 100 funds established by others at the MCF, CLICK HERE.

Thank you for your partnership in improving the quality of life for everyone in our community.

– Your staff at the Morton Community Foundation

Scott Witzig, Executive Director

Darcy Riddle, Administrative Manager

2024 Annual Spring Community Grant Cycle to distribute $91,000 to local agencies.

In 2023, the MCF's Annual Spring Community Grant Cycle distributed $75,000 in grants to local non-profit agencies, schools, parks and libraries to help them in the great work they do in and around our community. The photo above shows a crowd of children and parents awaiting their turn to compete in the Pumpkin Festival Big Wheel Race. The Morton Community Foundation provided a grant of a little over $1,700 to purchase new Big Wheel trikes for the race. The Pumpkin Festival Big Wheel Race is a fundraiser for Kids' Muddy Madness for St. Jude each year.

Thanks to the generosity of our donors, our endowment funds are growing, allowing us to grant more and more each year. The 2024 Spring Community Grant distributions will be $91,000. Wow! Just a few short years ago, we were distributing around $45,000. But, even more astounding is that, because of the fact that donations take about 4 years to fully "vest", we are able to project that if no additional gifts were donated, we will be distributing just under $127,000 in 2028. So, again, THANK YOU for your current donations as well as for the estate gifts that many of you are planning and/or have already planned. More on planned giving in this newsletter.

See the entire MCF Community Grant History from 2003 to 2023 HERE.

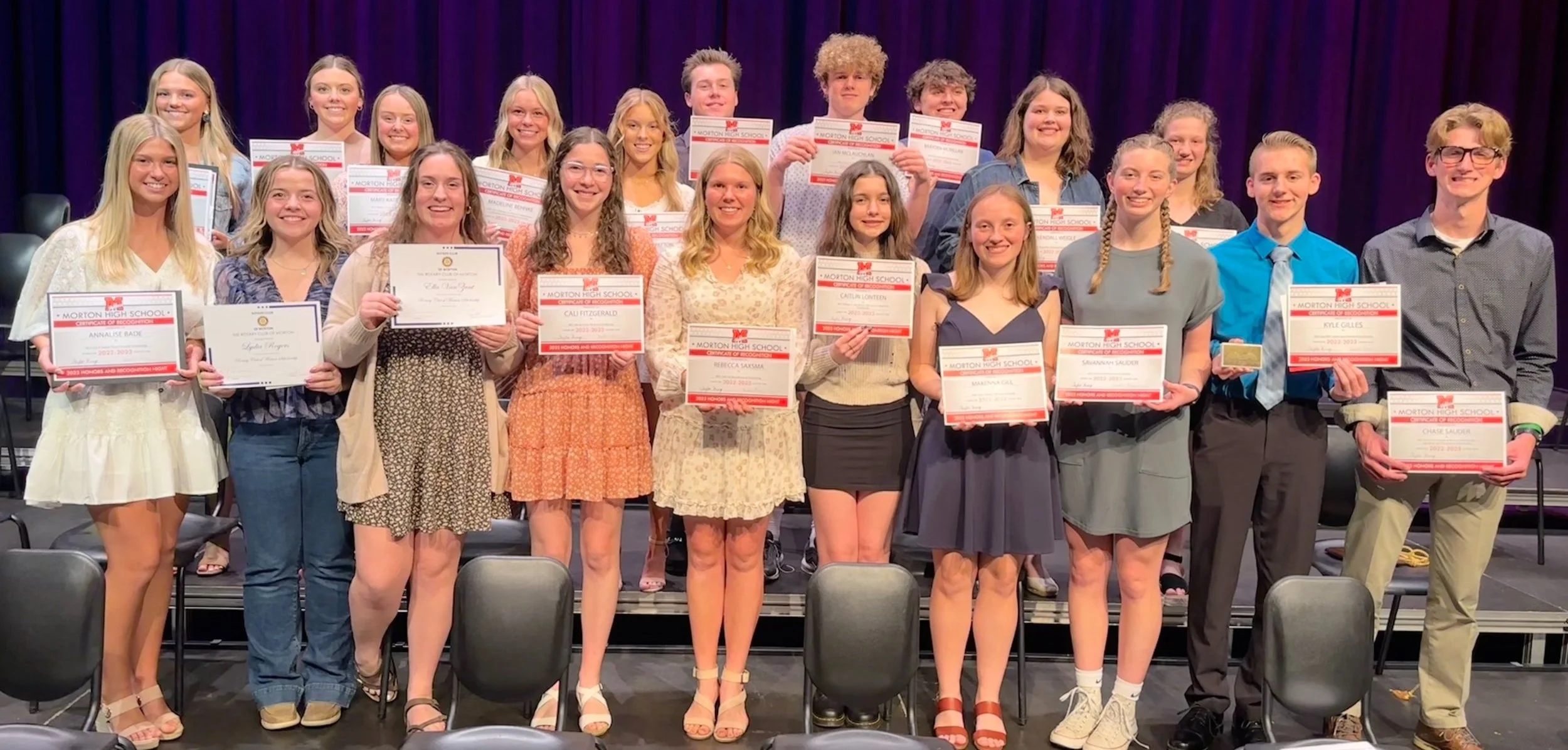

$36,225 in Scholarships available to Morton High School graduating Seniors

The photo above is the group of MHS Seniors who received scholarships in 2023. Morton High School Seniors can stop by the MHS Counseling office to pick up a packet of information about all 2024 scholarships available to them. The Morton Community Foundation is offering $36,225 in scholarship grants to qualified MHS students. If you know of a graduating senior, make sure they apply for one or more of these scholarships. There is a standardized application required for all scholarships, and then several scholarships also require an essay to be written. The deadline for scholarship applications is Tuesday, March 12. Read more about the available scholarships HERE.

Estate planning: One of the best ways to show you care

Money, mortality, and family relationships. Each of those topics alone can be tough for anyone to address head on, and when you combine them, it’s no wonder so many people put off setting up or updating their estate plans. Establishing a will, trust, and beneficiary designations forces a person to confront decisions about the ultimate division of their assets, and many people think estate planning is more expensive or more of a hassle than it really is.

But, getting your affairs in order–well before you need to due to age or illness–is truly a gift to your heirs. It’s extremely stressful for surviving spouses, children, and other loved ones to be faced with the emotional stress and workload of financial disorganization and uncertainty, on top of dealing with grief. Updating your estate plan also allows you to make arrangements for gifts upon your death to your favorite charities.

Many people choose to support their favorite charities in an estate plan through a beneficiary designation. As you work with your attorney and other advisors, be sure to review the beneficiary designations on your insurance policies and retirement plans. Pay close attention to tax-deferred retirement plans such as 401(k)s and IRAs. Typically, you’ll name your spouse as the primary beneficiary of these accounts to provide income following your death and to comply with legal requirements. But as you and your advisors evaluate whom to name as a secondary beneficiary of these tax-deferred accounts, don’t automatically default to naming your children or your revocable trust. You and your advisors may determine that naming a charity, such as your fund at the Morton Community Foundation, is by far the most tax-efficient, streamlined way to make gifts to your favorite causes upon your death and establish a philanthropic legacy. A bequest like this avoids not only estate tax, but also income tax on the retirement plan distributions.

Please reach out to the team at the community foundation as you work with your advisors on your estate plan. We can:

Review the many tax benefits of naming a fund/your fund at the Morton Community Foundation as a beneficiary of your IRA or other tax-deferred retirement account

Provide bequest language for your will or trust, properly describing your fund using the correct legal terms

Provide language for a beneficiary designation, again properly describing your fund using the correct legal terms

Work with you to update the terms of your donor-advised fund so that your wishes are carried out following your death, whether that is naming specific charities to receive distributions or naming your children as successor advisors to your fund

We’ve all heard stories about the sad consequences of someone not having an estate plan, or even having out-of-date beneficiary designations. Estate planning documents, including wills, trusts, and beneficiary designations, often turn out to represent generous acts of clear distribution and conflict avoidance. An estate plan allows you to demonstrate how much you care about the people in your life as well as your charitable passions.

Big or small, every gift matters

Simplicity, efficiency, and effectiveness have long been cornerstones of working with the Morton Community Foundation to carry out charitable goals. Time and time again at the MCF, we see how easily donors who’ve established a donor-advised or other type of endowment fund are able to not only fulfill their big-picture charitable goals, but to act quickly to respond to critical needs in the Morton area as they occur..

Indeed, the flexibility of working with the Morton Community Foundation allows you to support the causes you love at a financial level that meets your charitable giving budget. Early in the year, many of our fund holders transfer highly-appreciated stock to their donor-advised fund, for example, at the Morton Community Foundation so that they are prepared to activate their annual giving right away.

At every level of giving, philanthropy is a catalyst for improving quality of life. Indeed, anyone with a willingness to give can be a philanthropist. Whether you’re using your donor-advised fund to give $250 to a college or university, $2500 to a food bank, or $25,000 to an art museum’s endowment, you’re making a difference.

Consider that small donations from a large number of people can make a huge difference. This is especially true for responses to disasters and humanitarian tragedies. On the other end of the spectrum, very large donations to an organization can transform its ability to scale and serve a much greater population.

In so many ways, whether gifts are large or small or somewhere in between, philanthropy creates the margin of excellence that helps communities, families, and individuals thrive. The team at the MCF is here to help you achieve satisfaction and impact with your giving at any level.

What happens when I leave a bequest to my fund at the community foundation?

Many donors and fund holders at the Morton Community Foundation have updated their estate plans to leave a bequest to their donor-advised or other type of fund. You can set up a no obligation meeting with us to help you brainstorm all the options for leaving a legacy through the MCF.

Some bequests take the form of a “specific bequest,” which means that the fund at the community foundation receives a specific amount of money from the donor’s probate estate or trust. For example, for a specific bequest, your advisor might include a provision in your will as follows:

I bequeath $15,000 to The Community Foundation (taxpayer ID number and/or mailing address), a tax exempt organization under Internal Revenue Code Section 501(c)(3), to be added to the [Name of Your Fund], a component fund of The Community Foundation, and I direct that this bequest become part of the Fund.

In these situations the community foundation will be ready to receive your bequest, typically as soon as the estate is settled.

In other situations, you may want to leave a bequest of a portion of the remainder of your estate after all specific bequests, expenses, and taxes have been paid. These types of bequests are called “residuary” bequests. The language can look something like this:

I leave all the rest and residue of my property, both real and personal, of whatever nature and wherever situated, and assets, including all real and personal property, tangible or intangible, to The Community Foundation (taxpayer ID number and/or mailing address), a tax exempt organization under Internal Revenue Code Section 501(c)(3), to be added to the [Name of Your Fund], a component fund of The Community Foundation, and I direct that this bequest become part of the Fund.

Because the amount of a residuary bequest cannot be determined until all of the assets in an estate have been identified and valued, and all expenses and taxes have been paid, the designated charity (in this example, a fund/your fund at the community foundation) will not receive the full amount of a residuary bequest until the estate is completely settled. Typically, however, the estate’s personal representative or trustee will make what is known as a “partial distribution” to the residuary beneficiary (or beneficiaries as the case may be), as soon as the personal representative has enough information about the assets and liabilities to confidently do so.

Did you know you can leave a bequest that supports multiple funds at the MCF and/or charities…even if those charities are not located in Morton?

Many donors have created endowment funds either during their lifetime or through their estate plan that provide annual grants to multiple charities, even charities that are not located in Morton. For example, we have a fund established by a donor through her estate plan that annually grants to 8 charities, none of which are located in Morton. They’re all charities that the donor was passionate about during her lifetime. One of the 8 charities is the Crazy Horse Memorial in the Black Hills of southwestern South Dakota. We can accommodate grant distributions to any 501(c)(3) charity, or your alma mater, or your church…whatever your passion. Let’s have a conversation.

The team at the Morton Community Foundation looks forward to working with you and your advisors to establish bequests to fulfill your charitable legacies.